-

Palm oil, produced from the oil palm (Elaeis guineensis), constitutes approximately 30% of global vegetable oil production and is distinguished by exceptional land use efficiency, yielding far more oil per hectare than soybeans (Glycine max) while using a relatively small proportion of global oil-crop land to satisfy a large share of demand[1,2]. These agronomic advantages, however, coexist with a fundamental sustainability-related tension: The crop's economic success has historically been associated with deforestation, peatland conversion, and emissions from land use change. Beyond its environmental footprint, oil palm also has substantial socioeconomic and functional value. It is widely used in processed foods because of its oxidative stability and suitable melting characteristics, contributes important fatty acids and carotenoids, and supports millions of livelihoods in major producing countries[3,4].

As the world's second-largest importer, China has potentially significant leverage over governance of the palm oil supply chain[5,6]. Palm oil is widely used in the Chinese food industry, especially in instant noodles, baked goods, and fried snacks, and it is also used in cosmetics, detergents, and some industrial products[7,8]. Most of this palm oil is imported, primarily from Indonesia and Malaysia[1]. China has begun to engage more actively with sustainable sourcing initiatives, but the scope, consistency, and enforceability of this engagement remain limited[9].

China's Dual Carbon goals commit the country to peak carbon emissions before 2030 and achieve carbon neutrality before 2060[10]. Interim policy targets include lowering energy intensity and expanding the share of nonfossil energy, whereas long-term implementation relies on renewable energy deployment, carbon sinks, and carbon capture technologies[11,12]. This national decarbonization agenda intersects with a global carbon paradox: The expansion of oil palm cultivation in forests and peatlands can generate very high emissions from land use change[13,14]. In Indonesia, for example, peatland-based crude palm oil (CPO) production has been reported to have carbon footprints of around 26.0 t CO2 eq/t CPO, compared with about 5.7 t CO2 eq/t CPO under more conventional conditions[15]. These imported carbon risks are materially inconsistent with the mitigation logic of China's Dual Carbon strategy.

A number of governance and technological initiatives have been proposed to reduce these impacts. Certification under the Roundtable on Sustainable Palm Oil (RSPO), methane capture from palm oil mill effluent, and stronger traceability requirements are frequently presented as promising pathways[15,16]. However, the effectiveness of these measures remains contested. Voluntary certification does not always prevent deforestation, implementation costs can exclude smallholders, and external regulations such as the European Union's (EU's) Deforestation Regulation are reshaping the trade environment in ways that may create both incentives and tensions for producing countries[17]. China's growing market role therefore creates an opportunity for influence but is not an automatic guarantee of sustainability outcomes.

Recent literature has examined sustainable governance of palm oil, biomass utilization, and carbon dynamics, but the specific intersection between China's Dual Carbon goals and the global palm oil industry remains insufficiently explored. The key gap is not whether palm oil has been discussed, but how China's climate commitments may reshape governance, technology adoption, and carbon accounting across transnational supply chains. This review addresses that gap through three questions. (1) Which governance mechanisms are the most credible? (2) Which technological pathways are technically and economically realistic? (3) Under what land use conditions can palm systems generate genuine climate benefits?

-

A systematic literature search was conducted in October 2024 across four major databases—Web of Science, Scopus, China National Knowledge Infrastructure (CNKI), and Google Scholar—using keywords covering three thematic domains: palm oil ('palm oil' OR 'Elaeis guineensis' OR 'sustainable palm oil' OR 'CSPO' OR 'RSPO'), China-related terms ('China' OR 'Chinese' OR 'Sino-' OR 'Belt and Road' OR 'ASEAN'), and sustainability terms ('Dual Carbon' OR 'carbon neutrality' OR 'decarbonization' OR 'low-carbon' OR 'carbon sequestration' OR 'deforestation' OR 'land-use change' OR 'biofuel' OR 'biomass'). The search was limited to English and Chinese publications from 2015 to 2024, capturing the post-Paris Agreement period and the lead-up to China's 2020 Dual Carbon announcement.

Inclusion, screening, and analytical framework

-

Studies were included if they were peer-reviewed articles, conference proceedings, or authoritative reports from intergovernmental organizations (e.g., Food and Agriculture Organization, United Nations Environment Program, Intergovernmental Panel on Climate Change); addressed environmental, policy, or technological aspects of palm oil production, trade, or consumption; and were relevant to China's role in the palm oil supply chain or climate mitigation objectives. Studies focusing solely on domestic Chinese oil crops, nutritional or food science aspects without environmental relevance, or opinion pieces without institutional credibility were excluded. The initial search yielded 1,847 records; after removing duplicates, 1,435 titles and abstracts were screened, and 312 full texts were reviewed, resulting in 187 sources meeting the inclusion criteria. An additional 23 sources were identified via reference lists and institutional websites (e.g., RSPO, Council of Palm Oil Producing Countries (CPOPC), China Ministry of Ecology and Environment), producing a final corpus of 210 sources. The literature was analyzed using a thematic synthesis approach, organized into three main themes: governance pathways, including policy mechanisms, certification systems, and international cooperation initiatives evaluated for their effectiveness and implementation barriers; technological pathways, including low-carbon technologies, biomass utilization, and carbon sequestration potential assessed for technical feasibility, economic viability, and scalability; and barriers and enablers affecting the alignment between China's Dual Carbon goals and the palm oil sector across the policy, technological, and market dimensions. Within each theme, our analysis focused on opportunities, contested claims, trade-offs, implementation challenges, and evidence gaps, guided by a Global Production Network (GPN) perspective that frames China's Dual Carbon goals as an external 'shock' potentially reshaping governance dynamics across the global palm oil supply chain.

-

As one of the world's major consumers of palm oil, China requires stronger policy support for its low-carbon and green transition in the palm industry to maintain the sustainability of the global palm oil supply chain. First, the absence of mandatory green import standards and unified certification regulations poses a challenge. Unlike the EU's Deforestation Regulation and other compulsory policies, China's palm oil imports are still governed primarily by traditional inspection and quarantine standards, with sustainability indicators such as 'zero deforestation' and 'low carbon footprint' not included as prerequisites for market access. This allows palm oil with high environmental risks and lacking certification to legally enter the Chinese market[18]. The current certification rate for sustainable palm oil remains low, far below established targets, and there is a lack of incentives such as financial subsidies or tax relief. As a result, enterprises face high costs and risks in upgrading their supply chains and show limited motivation to do so[19]. Second, China's domestic Dual Carbon policies are disconnected from the global supply chain's dynamics. Current policies focus mainly on domestic sectors such as energy and industry, lacking a systematic management framework for 'embodied carbon' and carbon footprints in imported palm oil supply chains[20]. Corporate emission responsibilities are calculated only for the domestic processing stages, excluding carbon emissions from upstream overseas cultivation, thus creating a regulatory gap. Moreover, because of disparities in the Measurement, Reporting and Verification (MRV) standards and enforcement across provinces, China's carbon market suffers from weak pricing mechanisms and reduced incentive effectiveness, preventing the palm oil industry from benefiting from emissions trading. Additionally, green finance exerts limited constraints on overseas investments related to palm oil. Financial institutions often lack robust capacity for environmental–social–governance (ESG) due diligence, leading to capital flowing toward unsustainable production[21]. The lack of a consensus among stakeholders along the supply chain on a unified transition path, coupled with the absence of cross-sectoral coordination mechanisms, further hampers policy implementation.

Technological constraints

-

Technological bottlenecks also significantly constrain the low-carbon transition of China's palm industry, with core issues stemming from lagging application, insufficient research and development (R&D), and limited dissemination of low-carbon technologies. The uneven application of supply chain traceability technologies is particularly notable: Although leading enterprises have piloted blockchain and satellite-based remote sensing, the high costs hinder their widespread adoption among small and medium-sized enterprises. Furthermore, inconsistent data standards among different stakeholders have created 'data silos,' making it difficult to verify the source information and undermining the credibility of green certifications. The low level of digitization among smallholders also impedes full-chain traceability[22]. In processing, China lacks large-scale commercial palm oil extraction and refining facilities, relying instead on small-scale experimental setups. Technologies for the efficient utilization of empty fruit bunches (EFBs) and other waste biomass lag behind those in Malaysia and Indonesia, making it difficult to achieve economies of scale[23]. Many outdated factories operate with low energy efficiency and insufficient waste heat recovery, making them major sources of carbon emissions[24]. The development and commercialization of alternatives such as microbial oils are slow, confined to the laboratory stage, and face challenges including high costs, scalability difficulties, and stringent regulatory entry requirements. In addition, high-quality palm varieties have not undergone sufficient field trials or demonstration in South China, limiting their large-scale promotion. Low-carbon cultivation models, such as regenerative agriculture, have had few pilot studies in domestic production areas. Here, regenerative agriculture refers to management practices such as residue return, reduced soil disturbance, intercropping, and soil-carbon-enhancing cultivation strategies in perennial oil palm systems. The balance between technological feasibility and economic viability remains unclear, and the lack of demonstrative success weakens their ability to support a green supply chain transition[6].

Market and economic barriers

-

Market and economic barriers further constrain the alignment of China's palm oil supply chain with the Dual Carbon goals. The certification rate for sustainable palm oil remains relatively low, whereas financial incentives such as subsidies, tax relief, or preferential procurement policies are still insufficient to support large-scale transition. As a result, enterprises often face high compliance costs, supply chain upgrading expenses, and uncertain economic returns when attempting to adopt certified sourcing or low-carbon practices. In addition, green finance instruments have not yet exerted strong constraints on overseas investments related to palm oil, partly because financial institutions often lack robust ESG due diligence capacity and effective embodied carbon assessment tools. These weaknesses reduce market pressure for sustainability and allow capital to continue flowing toward environmentally risky production systems. At the same time, the commercial viability of many low-carbon technologies remains uncertain. Although traceability systems, biomass valorization, and alternative products may offer potential climate benefits, their large-scale deployment is often limited by high upfront costs, weak price competitiveness, and the absence of stable policy support. Together, these market and economic constraints slow the adoption of sustainable practices and weaken the overall transition potential of the palm oil supply chain in the Chinese context.

-

The collected literature was organized into three analytical themes: governance pathways, technological pathways, and barriers to alignment. The analysis further draws on the GPN perspective, treating China's Dual Carbon goals as an external policy signal that can influence standards, finance, sourcing behavior, and accountability across the palm oil supply chain.

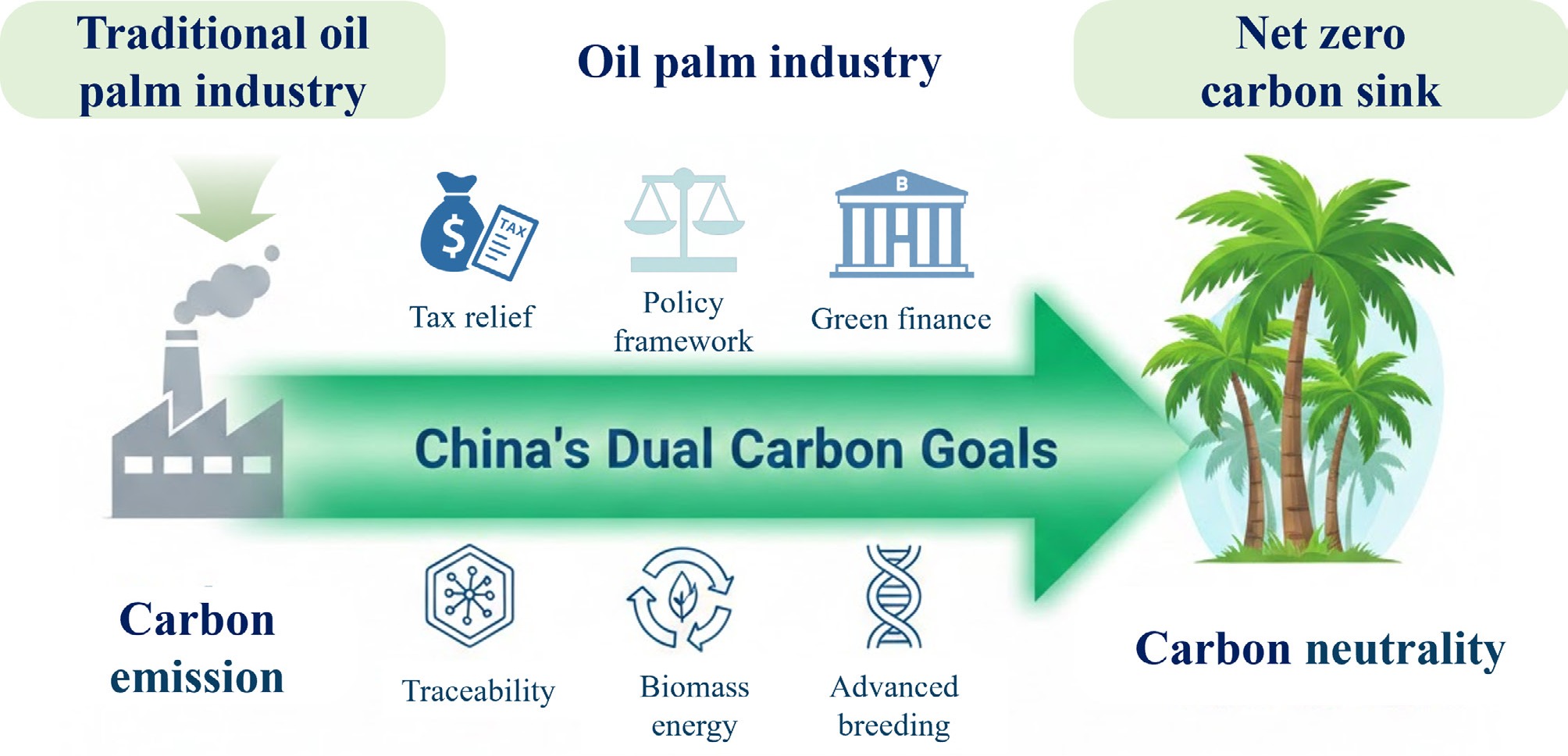

China's pursuit of its Dual Carbon goals (2030 as the emissions peak; 2060 as the goal for neutrality) necessitates leveraging strategic commodities like palm oil. This industry presents a paradox: its high yield (5 to 8 times more oil per hectare than soybeans) offers bioresource potential, yet traditional production drives 10%–15% of global emissions associated with land use change through deforestation and peatland degradation. Recent initiatives demonstrated how China is reconciling this tension through five integrated pathways, as shown in Fig. 1.

Figure 1.

Innovations in the governance of low-carbon technologies to build a sustainable oil palm Industry. The Yin–Yang metaphor is used to illustrate the dynamic balance between decarbonization opportunities and the environmental trade-offs associated with palm oil's development.

Barriers and pathways for a low-carbon palm oil supply chain in China

-

The RSPO, established in 2004, remains the best-known certification framework for sustainable palm oil. RSPO-certified production is intended to mitigate negative environmental and social impacts through standards on legality, transparency, environmental protection, and community rights, together with traceability systems such as identity preserved and mass balance[25]. By 2023, RSPO-certified plantations covered a substantial share of global production, indicating institutional scale but not necessarily uniform effectiveness across all landscapes[26]. China's engagement with RSPO has expanded, with growing membership, pilot traceable shipments, and stronger corporate commitments from leading brands. However, the environmental performance of certification should not be overstated. Existing studies report mixed outcomes: Certification may improve management and traceability in some contexts, yet the impacts on deforestation, biodiversity, and peat-related emissions remain uneven, especially where enforcement is weak or landscapes are already highly fragmented[27]. The relatively low penetration of certified sustainable palm oil in China, together with price premiums and smallholder entry barriers, limits the near-term transformative effect of certification alone.

Domestic policy instruments and international cooperation

-

Carbon markets, green finance, and preferential credit are frequently proposed as policy instruments that could support lower-carbon palm oil supply chains. Pilot experiences in southern China suggest that agroforestry or intercropping systems may be linked to carbon credit mechanisms, whereas green finance frameworks can, in principle, reward stronger environmental performance[28,29]. Even so, the direct applicability of these instruments to imported palm oil remains limited because current carbon accounting systems focus primarily on domestic emissions rather than embodied emissions in overseas production.

At the international level, China has engaged with cooperative initiatives such as the Global Framework Principles for Sustainable Palm Oil and has also influenced regional supply chains through trade, investment and the Belt and Road cooperation[30,31]. These channels offer opportunities for standard harmonization, technology transfer, and smallholder support but they also require a more critical assessment. Recent studies note that infrastructure and investment can simultaneously facilitate sustainability upgrades and resource expansion. Therefore, any claim that international cooperation is inherently green must be qualified by the strength of its safeguards, monitoring, and accountability mechanisms.

-

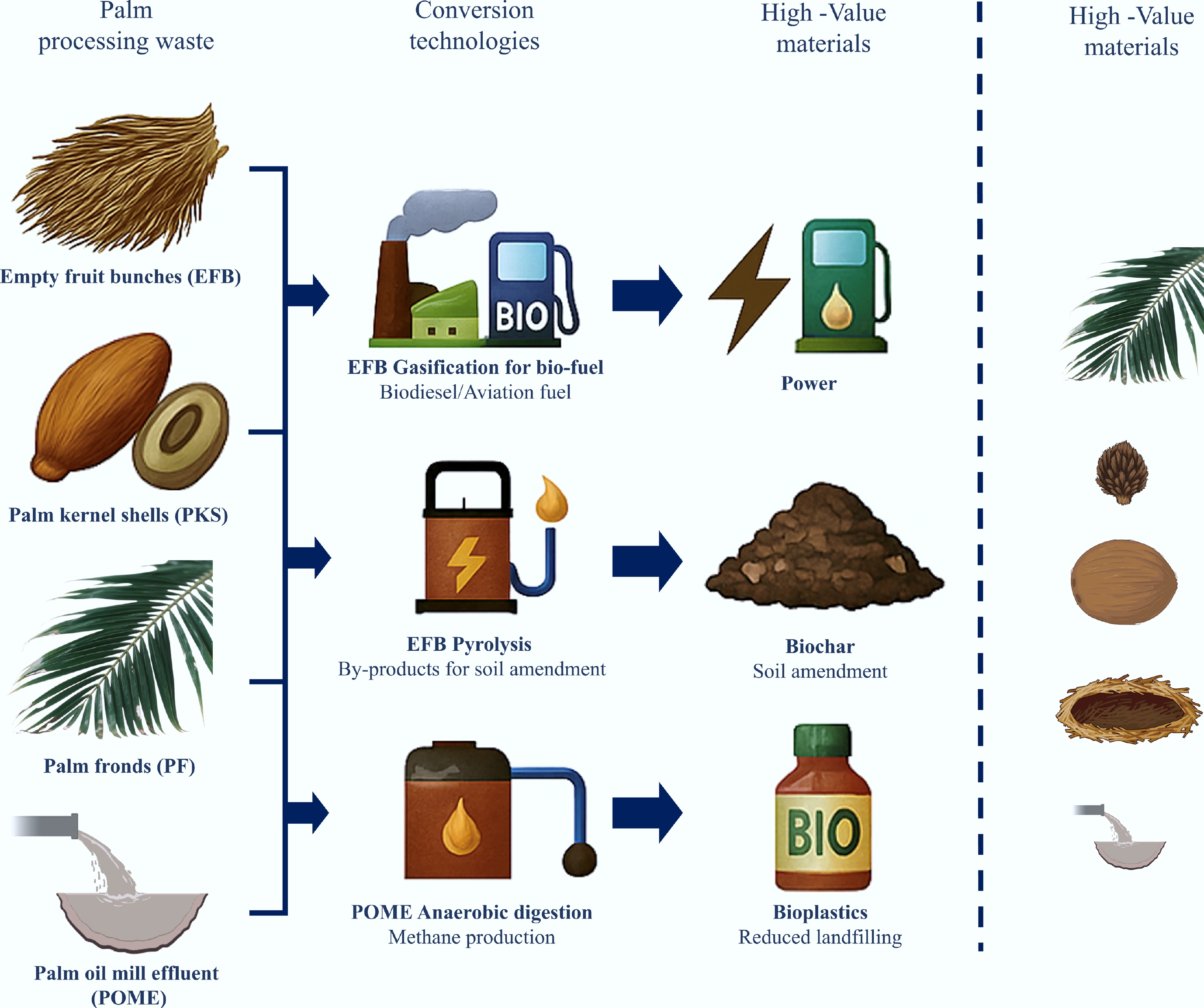

The palm oil industry, often criticized for its environmental impact, possesses significant yet under-realized potential to contribute to global decarbonization efforts through three interrelated pathways that underpin China's Dual Carbon objectives: the valorization of palm biomass residues as renewable energy, the intrinsic high-rate carbon sequestration capacity of Arecaceae species, and the continual development of derivative technologies (as demonstrated in Fig. 2). This section examines these dual facets, exploring established and emerging technologies for biomass conversion, the scientific basis for the crop's carbon sink capabilities, and ancillary technological advancements that support a more sustainable future for the industry. Technological innovation is frequently invoked as a route to align palm oil with climate goals. In practice, three pathways dominate the discussion: biofuel production and high-value by-products, valorization of biomass waste, and carbon sequestration in palm-based systems. These pathways differ substantially in their technological readiness, economic viability, and dependence on land use history, and they should therefore be assessed critically rather than treated as uniformly beneficial.

Figure 2.

Pathways for the valorization of palm biomass waste in a circular bioeconomy.

Scaling production and popularization of biofuel and other high-value by-products

-

Palm-based biodiesel can reduce lifecycle emissions relative to fossil diesel under certain production conditions, and pilot blending programs in China indicate policy interest in this route[32]. However, the size of the climate benefit depends strongly on the feedstock's origin. When palm oil is sourced from mineral soil plantations without recent deforestation, emission reductions may be substantial; when sourced from peatlands or newly cleared land, the carbon debt associated with land conversion can largely offset or even exceed the downstream biofuel benefits.

Beyond biodiesel, producer countries have expanded into higher-value derivatives such as glycerin, fatty acids, methane recovery, activated carbon, and bio-based materials[33]. China's downstream engagement remains comparatively limited, which constrains both its economic value capture and circular bioeconomy potential. Greater diversification could improve resource efficiency, but commercial scaling depends on the feedstock's availability, policy support, and the competitiveness of low-carbon products in domestic markets.

Popularization of palm biomass waste for renewable energy

-

Palm oil processing generates large volumes of residues, including EFBs, palm kernel shells, mesocarp fibre, and palm oil mill effluent, all of which can serve as feedstocks for energy and material recovery[34]. Reported pathways include pelletization, co-firing, biogas capture, gasification, and biochar production[35−37]. These options can reduce waste, substitute for fossil fuels, and, in some cases, improve carbon retention through the incorporation of biochar.

Emerging conversion technologies promise greater efficiency. Gasification of residues like EFBs and pruned palm fronds (with calorific values of 18–20 MJ kg−1) enables the production of syngas for highly efficient electricity generation[38]. Integrated gasification combined cycle (IGCC) systems adapted for palm biomass achieve over 30% emission reductions compared with traditional grid electricity or conventional power generation, positioning them as critical for decarbonizing rural energy systems[39]. Among the palm crops, coconut waste also exhibits high potential as a feedstock for biofuels, alongside oil palm. Briquettes made from old coconut waste reached a calorific value of 6.927 kcal g−1 (approximately 29 MJ kg−1) after 90 min of carbonization[40]. Specifically, coconut shells have a calorific value of 17.40 MJ kg−1 and the husks have 10.01 MJ kg−1. These values are similar to some wood species and suggest their potential for use as biofuels[41]. Moreover, charred coconut waste has a 42% higher calorific value than uncharred waste, highlighting the benefits of controlled biochar production[42]. Nevertheless, technical feasibility does not automatically imply economic viability. Commercial deployment often requires high upfront investment, reliable residue collection, supportive electricity pricing or fuel markets, and clear carbon policy incentives. In China, an additional constraint is that most palm biomass residues are generated overseas, which limits the extent to which their energy value can be directly captured domestically unless cooperative processing and supply arrangements are established with the producer countries.

Carbon sequestration in Arecaceae systems

-

The discussion of carbon sequestration using oil palm must begin with an essential caveat: Climate benefits are highly context-dependent and temporally bounded. Net gains are plausible when palms are established on degraded land or when management practices increase biomass and soil carbon without displacing high-carbon ecosystems. By contrast, conversion of forests or peatlands creates large initial emissions and long carbon payback periods. The Arecaceae family demonstrates exceptional carbon sequestration capabilities. Their extensive and deep fibrous root systems are crucial for long-term carbon storage, significantly enhancing belowground soil organic carbon (SOC) stocks. Aboveground, these crops exhibit high net primary productivity, efficiently converting atmospheric CO2 into substantial biomass. Their fruits—rich in energy-dense lipids and carbohydrates—represent a significant form of sequestered carbon. For instance, the high oil yield of oil palm and the sugar-rich flesh of dates (Phoenix dactylifera) are essentially concentrated carbon sinks. Therefore, the strategic and sustainable cultivation of diverse palm species on suitable lands can markedly increase terrestrial carbon storage.

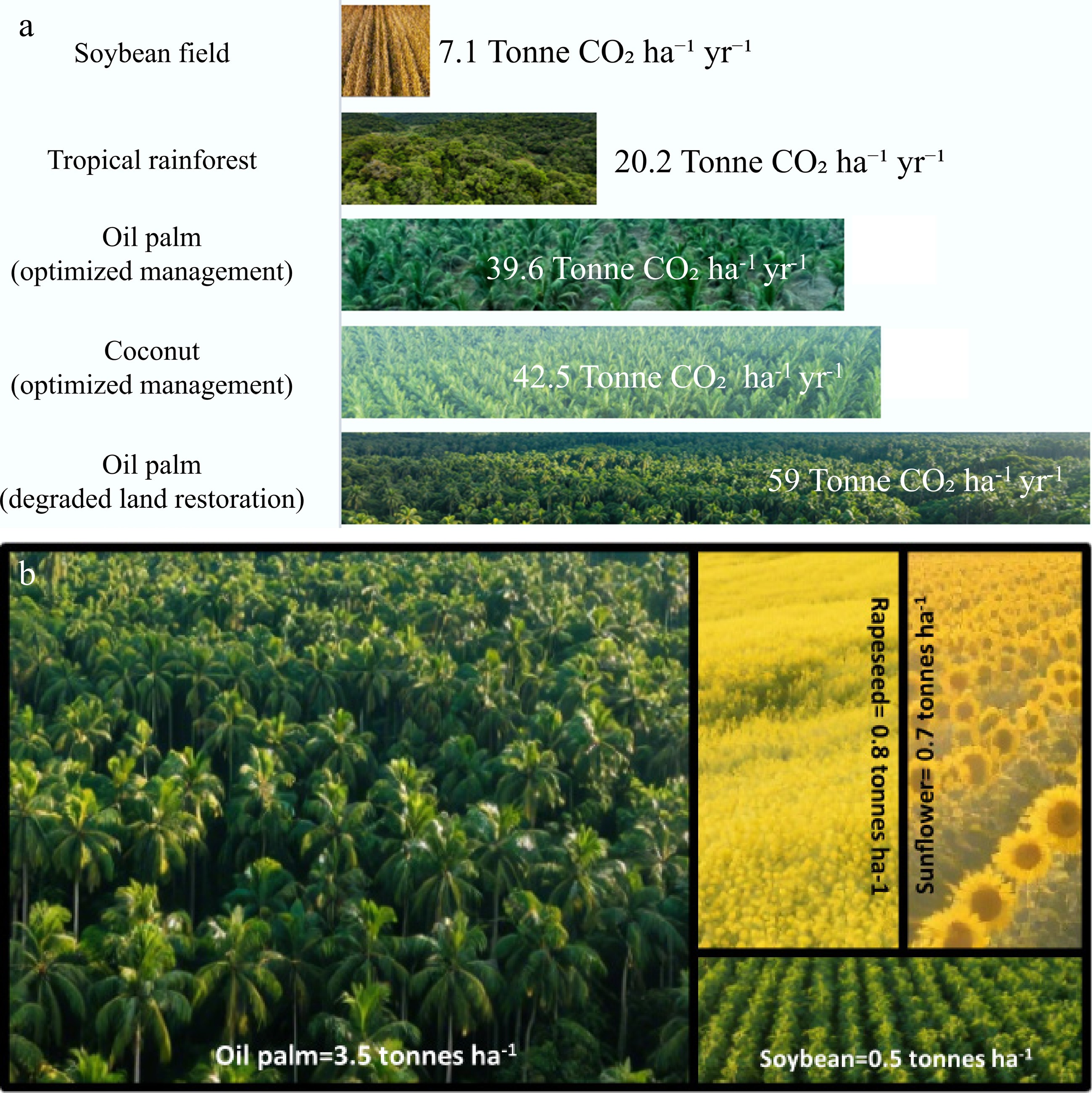

Oil palm and related palms can accumulate substantial biomass and may function as temporary carbon sinks during their productive growth phases, reflecting relatively high net primary productivity[43−45]. However, the magnitude of this climate benefit varies substantially across studies, depending on the plantation's age, land use history, management regime, and accounting boundaries. Under relatively favorable conditions, annual carbon sequestration is more conservatively estimated at approximately 20–30 t CO2 ha−1 yr−1, rather than the much higher values sometimes reported in site-specific or gross uptake calculations (Fig. 3). Claims that oil palm is a superior carbon sink therefore require careful qualification with respect to the time horizon, baseline land use, and whether estimates represent gross annual uptake or the net carbon balance over an entire rotation cycle. Replanting, soil disturbance, and prior land conversion can materially alter these factors.

Figure 3.

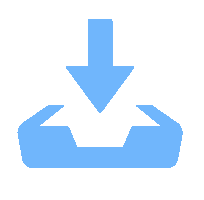

Carbon sequestration potential and oil yield of oil palm versus other crops and ecosystems. (a) Comparison of carbon sequestration capacities among different crops and ecosystems; the value of oil palm shown represents an approximate annual range under specific land use and management conditions rather than a universal value across all plantation systems. (b) Comparison of oil yield among different oil crops, where the size of the squares corresponds to actual oil yield capacity.

Circular residue management can strengthen the carbon performance of palm systems. Returning pruned fronds or EFBs to the field has been shown to improve SOC, nutrient cycling, and long-term soil conditions[46,47]. For southern Chinese regions such as Hainan, Guangxi, Guangdong, and Yunnan, any discussion of expanding palm oil production should remain cautious and conditional. Potential carbon sink benefits must be weighed against ecological risk, water demand, biodiversity concerns, and the economic reality that local production conditions differ from those in Southeast Asia[48].

-

Advances in low-carbon-related technologies are pushing the transition in the palm oil industry. In the biofuel sector, national blending mandates such as Indonesia's B40 and Malaysia's B20 utilize transesterification[49] and hydrodeoxygenation techniques to produce EN 14214-compliant biodiesel and renewable hydrocarbon fuels, significantly reducing reliance on fossil diesel and aiding emission mitigation efforts. Concurrently, blockchain-enabled traceability systems are being developed to establish transparent, immutable records of palm oil supply chains, enabling traceability from plantations to the end consumers and enhancing certification processes; for example, a proposed model in Indonesia integrates smart contracts and geospatial imaging to ensure verifiable sustainability claims[50]. Synthetic biology innovations are deploying genetically engineered microorganisms and enzymatic hydrolysis to convert palm oil residues into high-value bio-based products. One study demonstrated the successful transformation of palm oil mill effluent into biojet fuel using enzymatic hydrolysis followed by catalytic upgrading, showcasing both environmental and economic benefits[51]. Thus, these innovations and derivative technological advances constitute a tripartite foundation for low-carbon transformation. Future progress will depend less on technological optimism alone than on the practical alignment of readiness, cost, and governance. Near-term priorities should focus on scaling measures that are already relatively mature, such as better certification uptake, stronger traceability, methane capture, and feasible biomass valorization. These are more immediately actionable than speculative solutions whose deployment horizons remain long.

Digital traceability systems, precision agriculture, molecular breeding, and omics-assisted improvement may all contribute to lower-carbon production, but their adoption in the palm oil sector faces real constraints, including data fragmentation, high transaction costs, long breeding cycles, and uncertain field performance[52,53]. In particular, proposals for cold-resistant oil palm and northward expansion in China must be treated cautiously because they raise ecological, agronomic, and regulatory questions that are not yet resolved.

Advanced biofuels and high-end oleochemicals may offer useful niche opportunities, but their aggregate climate contribution is likely to remain modest unless backed by sustained policy incentives and clear sustainability criteria[35,54]. A realistic roadmap therefore prioritizes interventions with higher present feasibility and clearer governance support over those that remain technically interesting but commercially distant.

-

This review argues that alignment between the global palm oil industry and China's Dual Carbon goals is possible only under a more stringent governance and evidence framework than is often implied in optimistic narratives. Certification, biomass valorization, traceability, and policy coordination each offer partial solutions, but none is sufficient on its own. Their effectiveness depends on enforceable standards, transparent monitoring, economically viable implementation pathways, and explicit safeguards against deforestation and peatland conversion.

Three priorities emerge. First, China should strengthen its green procurement and traceability requirements for imported palm oil, with particular attention given to deforestation-free sourcing and stronger smallholder inclusion. Second, carbon accounting and green finance tools should be developed more carefully for transnational agricultural supply chains, including clearer methodological links to embodied emissions and verified mitigation outcomes. Third, research and investment should prioritize technologies with near-term feasibility, especially methane capture, biomass recovery, and practical traceability systems, treating more speculative options with appropriate caution.

Finally, digital traceability platforms—powered by blockchain and IoT sensors—can deliver end-to-end transparency, ensuring that every drop of palm oil imported into China meets both the environmental and social benchmarks. By converging precision agriculture, advanced breeding, biorefinery technologies, carbon credit incentives, and robust supply chain governance, the palm oil sector can transcend its historical carbon footprint to become a flagship example of a resilient, low-carbon agro-industry, aligning commodity production with biodiversity conservation and rural livelihoods under China's overarching climate pledge. Under these conditions, China's Dual Carbon goals could become a meaningful lever for improving the climate performance of the palm oil supply chain. Without them, the gap between climate ambition and commodity-supply reality will persist.

All authors thank Hainan Seed Industry Lab and Sanya Kelaite Co., Ltd. for their important support.

-

Not applicable.

-

The authors confirm their contributions to the paper as follows: Study conception and design: Mu Z, Ma Y; information collection: Yang S, Wimalasiri E; draft manuscript preparation: Yang S, Wimalasiri E; presentation of graphs: Yang S, Mu Z, Yang Z; review of manuscript: Yang Z, Mu Z. All authors reviewed the results and approved the final version of the manuscript.

-

All data used in this review were derived from published literature and institutional sources accessible through Qinghai University and Hainan University. No new datasets were generated for this review, and all information used is available, subject to the access conditions of the original sources.

-

This paper was sponsored by Sanya Yazhou Bay Science and Technology City (Grant No. SCKJ-JYRC-2024-35) and Hainan Technology and Innovation Project for Talent (Grant No. KJRC2023L09).

-

The authors declare that they have no conflict of interest.

-

# Authors contributed equally: Shuya Yang, Yinghao Ma

Full list of author information is available at the end of the article. - Copyright: © 2026 by the author(s). Published by Maximum Academic Press, Fayetteville, GA. This article is an open access article distributed under Creative Commons Attribution License (CC BY 4.0), visit https://creativecommons.org/licenses/by/4.0/.

-

About this article

Cite this article

Yang S, Ma Y, Hao S, Wimalasiri EM, Yang Z, et al. 2026. Integrating the palm oil industry into China's Dual Carbon goals: governance and technological pathways. Agricultural Ecology and Environment 2: e012 doi: 10.48130/aee-0026-0011

Integrating the palm oil industry into China's Dual Carbon goals: governance and technological pathways

- Received: 21 January 2026

- Revised: 11 March 2026

- Accepted: 13 April 2026

- Published online: 21 April 2026

Abstract: The palm oil industry, which supplies approximately 30% of global vegetable oil while using a relatively small share of oil-crop land, sits at the center of a major carbon dilemma. Although the sector contributes to food security and rural livelihoods in Southeast Asia, its historical expansion has been associated with deforestation, peatland degradation, and substantial greenhouse gas emissions. This review examines under what conditions the global palm oil industry can align with China's Dual Carbon goals. We synthesize evidence on three interconnected dimensions: governance mechanisms and their trade-offs, the technical and economic viability of low-carbon technologies, and the context-dependent nature of carbon sequestration in palm systems. The analysis suggests that certification, green procurement, biomass valorization, and regional policy coordination can support decarbonization, but their effectiveness remains limited by fragmented regulation, weak traceability, uneven smallholder inclusion, and unresolved carbon accounting issues. We argue that net climate benefits are plausible only when sustainable palm oil expansion avoids high-carbon ecosystems and is linked to robust governance, transparent monitoring, and economically viable low-carbon technologies.